Have you ever filled a prescription only to find out the pharmacy wants $5 for one version of the drug and $150 for another? It feels like a random penalty, but it’s actually a calculated move by your insurance company. They use something called preferred generic lists, which are part of a larger system known as insurance formularies that categorize drugs into tiers based on cost and effectiveness. These lists dictate exactly which medications get the lowest copays and which ones will drain your wallet.

Understanding why insurers prefer certain products isn't just about saving money-it's about knowing how the healthcare system is designed to shift costs. Insurance companies don't pick drugs at random. They rely on data, negotiations, and strict rules to push patients toward specific options. If you want to keep your monthly bills low, you need to understand the mechanics behind these choices.

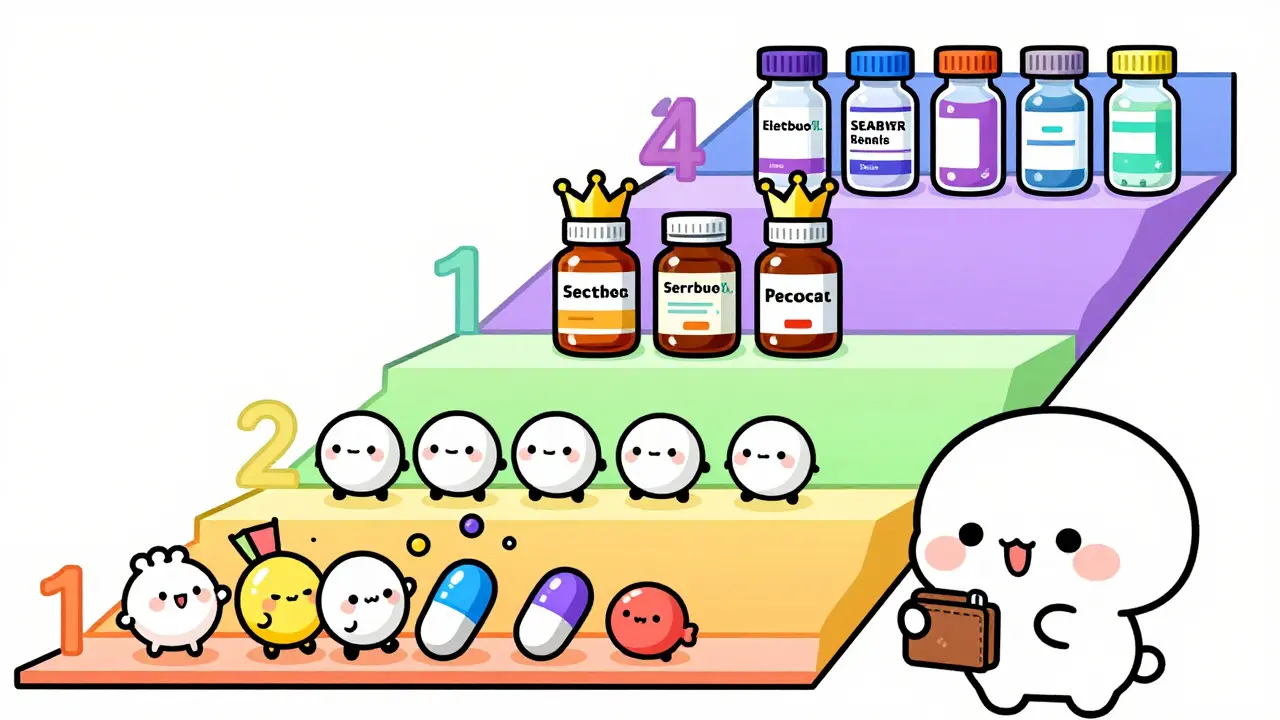

How Formulary Tiers Work

Your insurance plan doesn't treat all drugs equally. Instead, it uses a tiered structure. Think of it like airline seating: economy, premium economy, business class, and first class. The lower the tier, the less you pay out of pocket.

| Tier | Type of Drug | Estimated Copay (30-day supply) |

|---|---|---|

| Tier 1 | Preferred generics and biosimilars | $5 - $15 |

| Tier 2 | Non-preferred generics or preferred brands | $25 - $50 |

| Tier 3 | Non-preferred brand-name drugs | $50 - $100+ |

| Tier 4 | Specialty drugs (biologics) | $100+ or % coinsurance |

Tier 1 is where the preferred generic list lives. These are drugs that have lost their patent protection and can be made by multiple manufacturers. Because competition is high, prices drop significantly. According to FDA data from 2022, generic drugs typically cost 80-85% less than their brand-name counterparts. When six or more companies make the same generic, prices can fall by up to 95%. Insurers love this because it lowers their overall spending, which allows them to offer lower premiums to everyone.

If your doctor prescribes a Tier 1 drug, you pay almost nothing. If they prescribe a Tier 3 brand name, you might pay hundreds. This gap is intentional. It forces patients and doctors to consider cheaper alternatives first.

The Role of Pharmacy Benefit Managers (PBMs)

You might wonder who decides which drugs go on the preferred list. It’s not usually your insurance company directly. It’s a middleman called a Pharmacy Benefit Manager (PBM), a company that manages drug benefits for health plans by negotiating prices with pharmacies and manufacturers.

PBMs like CVS Health, Cigna’s Evernorth, and UnitedHealth’s OptumRx control nearly 78% of the market. Their job is to negotiate rebates from drug manufacturers. Here’s the catch: PBMs often get higher rebates from brand-name drug makers than from generic makers. So, why do they still push generics?

It comes down to volume and stability. While a brand-name drug might offer a nice rebate check to the PBM, the base price is still high. Generics have such low base prices that even without massive rebates, they save the insurer money overall. Plus, having a predictable, low-cost option reduces administrative headaches. PBMs secure average rebates of 25-30% on brand names, but direct purchasing agreements for generics create a stable, low-cost floor for the entire formulary.

Why Your Doctor Might Disagree

This system creates tension between insurers and physicians. Doctors care about what works best for their individual patient. Insurers care about what works best for the population as a whole.

Scott Glovsky, an insurance specialist, points out that physician decisions are often questioned by people who don’t understand unique patient circumstances. For example, some patients react poorly to specific inactive ingredients in generic versions of a drug. Even though the active ingredient is identical, the filler or dye might cause issues. In these cases, the doctor wants to prescribe the brand name, but the insurer says no unless you prove the generic failed.

This leads to "step therapy" protocols. Step therapy means you must try the preferred generic first. If it doesn’t work, then-and only then-will the insurer cover the brand name. The American Medical Association reported in 2022 that 42% of physicians experienced treatment delays due to these protocols, particularly in chronic pain management. It’s a frustrating process that can leave patients suffering while paperwork gets sorted out.

Biosimilars: The New Frontier

Generics aren’t just for pills anymore. Complex biological drugs, used for conditions like rheumatoid arthritis or Crohn’s disease, now have copies too. These are called biosimilars, which are highly similar biologic medical products already approved by regulatory agencies.

Insurers are pushing hard to put biosimilars on their preferred lists. However, adoption is slow. In Europe, 85% of eligible biologic prescriptions switch to biosimilars. In the U.S., that number was only 15% in 2023. Why the difference?

Brand-name biologic manufacturers often offer co-pay assistance cards that bring patient costs down to zero. Biosimilar manufacturers haven’t always matched this strategy. As a result, a patient might see a lower list price for the biosimilar but end up paying more out of pocket because there’s no manufacturer discount card. This confuses patients and discourages doctors from switching.

To fix this, Medicare’s 2024 final rule requires Part D plans to place biosimilars in the same tier as reference biologics starting in 2025. This policy change aims to boost biosimilar utilization from 15% to 45%, making expensive treatments more accessible.

How to Navigate Preferred Lists Yourself

You don’t have to accept the default path. You can actively manage your medication costs by understanding your formulary. Here are practical steps to take:

- Check the tier before you fill: Most insurance apps let you look up a drug’s tier. If your doctor prescribes a Tier 3 drug, ask if a Tier 1 generic exists. A simple conversation could save you hundreds.

- Ask about "Dispense as Written": In 89% of states, pharmacists can automatically substitute a generic unless the doctor writes "dispense as written." If you prefer the brand, you need to know this option exists. Conversely, if you want the cheapest option, ensure your doctor hasn’t blocked substitution unnecessarily.

- Appeal denials: If your insurer denies a brand-name drug, you can appeal. According to Kaiser Family Foundation data, 68% of appeals succeed when a physician provides documentation proving therapeutic necessity. Don’t give up after the first "no."

- Review annually: Formularies change every year. A drug that was Tier 1 last year might move to Tier 3 next year. During open enrollment, check if your current medications are still preferred. Switching plans might be cheaper than staying put.

Patients who actively engage with their formulary structures reduce medication costs by an average of 32%. It takes about 45 minutes of research per year, but the savings are significant.

The Future of Drug Pricing

The landscape is shifting. The Inflation Reduction Act of 2022 introduced a $2,000 annual out-of-pocket cap for Medicare Part D by 2025. This cap changes the dynamic. Previously, insurers had little incentive to help patients once they hit high costs because the patients bore the burden. Now, insurers share the risk, so they are more motivated to steer patients toward preferred generics to keep total costs down.

We’re also seeing the rise of "Value-Based Formularies." UnitedHealthcare announced in early 2024 that it would dynamically adjust tier placement based on real-world effectiveness data. This means a generic might move up a tier if data shows it causes more side effects, or a brand might drop down if it proves superior in long-term outcomes. The goal is to move beyond simple cost-cutting toward true value-based care.

By 2030, experts predict that tier placement will be determined largely by outcomes data rather than cost alone. Until then, understanding the current system is your best defense against surprise bills.

What is a preferred generic list?

A preferred generic list is a subset of an insurance formulary containing generic drugs that offer the lowest out-of-pocket costs to patients. These drugs are placed in Tier 1 because they are therapeutically equivalent to brand-name drugs but cost significantly less due to market competition.

Why does my insurance require me to try a generic first?

This practice is called step therapy. Insurers use it to ensure that cheaper, effective alternatives are tried before covering expensive brand-name drugs. It helps control overall healthcare costs, though it can sometimes delay access to preferred treatments.

Can I refuse a generic substitution?

Yes, but it may cost you more. You can ask your doctor to write "dispense as written" on the prescription, or inform the pharmacist you want the brand name. Be prepared to pay the higher copay associated with non-preferred or brand-name tiers.

Are generics as safe as brand-name drugs?

Yes. The FDA requires generics to demonstrate bioequivalence within 80-125% of the brand-name product’s pharmacokinetic profile. Research shows therapeutic equivalence in 98.5% of generic approvals, making them a safe and effective alternative for most patients.

What happens if a preferred generic causes side effects?

If a preferred generic causes adverse reactions, your doctor can file an appeal with your insurer requesting coverage for the brand-name drug. Success rates for such appeals are around 68% when supported by proper medical documentation.

How do PBMs influence which drugs are preferred?

PBMs negotiate rebates and pricing with manufacturers. They place drugs on preferred lists based on a combination of low acquisition cost, negotiated rebates, and clinical efficacy data. Their goal is to minimize the total cost of drug benefits for the insurance plan.